Datadog Stock Is Up +66%. Here Are 5 Reasons Why, And Why It’s the Cleanest AI Beneficiary in B2B.

Акции Datadog выросли на 66% с начала 2026 года, а капитализация достигла $79 млрд — компания стала одним из главных бенефициаров ИИ-бума в B2B-секторе. В первом квартале 2026 года Datadog впервые преодолела отметку $1 млрд квартальной выручки, ускорив рост до 32% год к году при ARR свыше $4,2 млрд. Чистое удержание выручки (NRR) вернулось к 120%+, а рост выручки от не-ИИ клиентов ускорился до середины двадцатых процентов, что доказывает: ИИ увеличивает спрос на наблюдаемость всей инфраструктуры, а не только ИИ-нативных нагрузок. Бронирования новых клиентов более чем удвоились год к году, включая крупнейшие ИИ-лаборатории мира — предположительно, Anthropic стала рекордным новым клиентом квартала. Мультипродуктовый подход укрепляет позиции: 35% клиентов используют 6+ продуктов, а 5 продуктов приносят более $100 млн ARR каждый. Годовой прогноз повышен на $240 млн после одного квартала, а свободный денежный поток составил $289 млн при марже FCF 29%.

Datadog Stock Is Up +66%. Here Are 5 Reasons Why, And Why It’s the Cleanest AI Beneficiary in B2B.

by | 5 Interesting Things, Blog Posts, Scale

Guess Whose Stock Is Up +66% year-to-date? And trades at 20x ARR? In the midst of the most challenging run for software stocks … ever?

Datadog.

As of May 22, 2026: $222.32 per share, +66.20% year-to-date. Market cap: $79B. 52-week low was $98.01 just months ago. 52-week high is right now.

Why?

They’ve leaned into the AI Beneficiaries. Deeply.

Datadog isn’t an AI company — at least, not in the sense of the LLMs and AI native software leaders. They monitor and secure everything else. And it turns out that being the picks-and-shovels platform underneath every AI workload (plus every traditional workload that AI is making more complex) is one of the best trades in B2B right now.

Q1 2026 was the proof. Datadog just crossed $1B in quarterly revenue for the first time. And they did it the hard way: by accelerating growth, not decelerating. The stock popped 30%+ on the print and hasn’t looked back (CNBC).

Datadog has long been a bellwether for cloud infrastructure spend. Now it’s becoming the bellwether for something bigger: AI as a tailwind that lifts every workload, not just AI-native workloads.

Here are the 5 most interesting learnings:

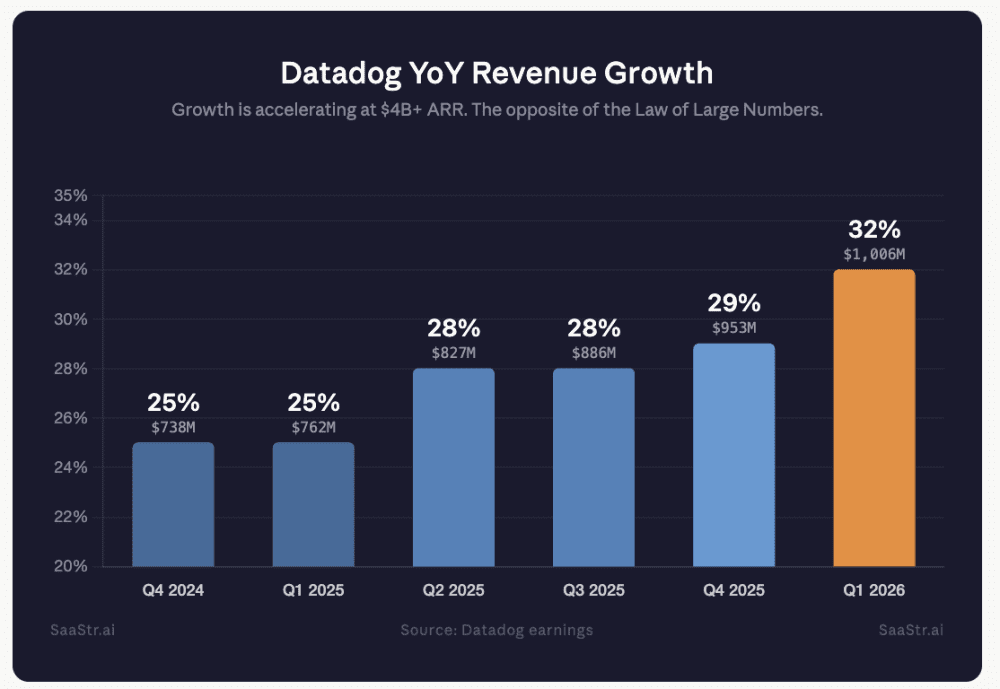

#1. Growth ACCELERATED at $4B+ ARR. From 25% to 32%. Almost Nobody Does This.

Datadog grew 32% YoY in Q1 2026 to $1.006B in quarterly revenue. That’s $4.23B in ARR (Datadog Q1 2026 Press Release).

What’s wild isn’t the absolute number. It’s the trajectory. Six straight quarters of acceleration:

Growth accelerated from 29% last quarter and 25% in the year-ago quarter (Q1 2026 Earnings Transcript). Almost no public B2B company at $4B+ ARR sees growth accelerate by 700 basis points in a year. The Law of Large Numbers should be kicking in hard by now. Datadog is doing the opposite.

This is what happens when a platform sits in front of a brand new workload (AI), AND the old workloads (cloud + apps) keep growing too.

#2. NRR Is Back to 120%+. From High-110s a Year Ago. The Optimization Era Is Over.

This is the cleanest signal on the print.

Net Revenue Retention had drifted into the 110s through 2024 and 2025 as customers (especially cloud-natives) optimized usage. The bear case was that this was the new normal.

Per the Q1 2026 10-Q:

“As of March 31, 2026, our trailing 12-month dollar-based net retention rate was low-120%’s. As of March 31, 2025, our trailing 12-month dollar-based net retention rate was high-110%’s. The increase in our trailing 12-month dollar-based net retention rate was attributable to increased usage growth from existing customers.” (Datadog 10-Q Q1 2026)

Customers aren’t optimizing anymore. They’re consuming. New apps, more telemetry, more AI workloads, more everything. That’s a 4-point swing on a $4B base. Massive.

#3. NON-AI Customers Are Growing Faster Too.

Everyone assumes “AI revenue” at Datadog = AI-native customers (OpenAI, Anthropic, the big labs).

It’s the opposite.

Non-AI customer revenue growth also accelerated to mid-20% YoY, up from 23% last quarter and 19% in the year-ago quarter (Q1 2026 Earnings Transcript).

Meanwhile, the AI-native cohort (which includes their largest customer) grew only high single digits YoY in Q1 2026 (Datadog 10-Q Q1 2026). Optimization is real in that cohort.

The real AI Beneficiary thesis: AI is making every company ship more code, deploy more apps, generate more telemetry. Traditional enterprises are building agents. They’re spinning up GPU clusters. They’re running inference. And every one of those workloads needs to be monitored.

AI doesn’t just create demand for AI-native infrastructure. It creates demand for all infrastructure observability. That’s the trade.

#4. The Multi-Product Moat Is Getting Stronger. 35% of Customers Now Use 6+ Products.

A year ago, the multi-product adoption stats looked like this:

Today:

The 8+ product cohort grew 54% relative YoY. That’s where the deepest stickiness lives.

Of Datadog’s 26 products: 5 generate over $100M in ARR each, 3 more are between $50-100M, and 18 are still early in their lifecycle.

For founders: this is the platform playbook done right. Land with one wedge (infrastructure monitoring). Expand into adjacent telemetry (logs, APM, security, RUM, GPU monitoring, LLM observability, security agents). Each new module raises NRR and increases switching costs. 18 of the 26 products still being early-stage means there’s a lot of expansion ARR still to come.

#5. New Logo Bookings MORE THAN DOUBLED YoY. The AI Labs Themselves Are Now Buying.

Everyone focuses on expansion at Datadog. The new logo story was the most under-discussed beat of the quarter.

New logo annualized bookings set an all-time record and more than doubled year over year, including large deals in observability, security, and data products. The bookings spanned wins in “newer products like security, Data Observability, and Flex Logs” (Q1 2026 Earnings Call).

That includes new land deals with two of the world’s biggest AI research teams, helping them improve and optimize their training workflows.

And the AI labs themselves are now choosing Datadog over building in-house.

Per Hunterbrook’s analysis of the call, the largest “new logo” in Datadog’s history was consolidating onto Datadog from a fragmented mix of “more than five open-source, commercial, hyperscaler, and in-house” tools. They make a compelling case that this is Anthropic, since OpenAI is already Datadog’s biggest customer (and thus not a new logo), and Grafana Labs publicly named Anthropic as a customer in September 2025, supplying exactly the kind of open-source observability tooling Pomel said the customer was migrating away from (Hunterbrook).

Which AI Leaders Use Datadog

Pulling from earnings calls, public integrations, and analyst commentary:

Datadog’s own State of AI Engineering report (built from its customer telemetry) found that more than 70% of organizations now use 3+ models, and the share using 6+ models nearly doubled in the last year. Teams are building model portfolios, not picking a single default. Every one of those portfolios needs observability.

Total $100K+ ARR customers: ~4,550, up 21% from ~3,770 a year earlier (Q1 2026 Press Release).

Translation: at $4B ARR, Datadog isn’t running out of new logos. It’s getting more of them than ever, faster than ever. The TAM keeps expanding because AI keeps creating new categories of things to monitor.

Bonus: Datadog Raised Full-Year Guidance by $240M After One Quarter

FY2026 guidance moved to $4.30-$4.34B, up from prior guidance of $4.06-$4.10B in February. A $240M raise after one quarter. That’s confidence.

Q2 revenue is expected at $1.07B-$1.08B, which implies further sequential acceleration (Alpha Spread).

Combined with $289M in free cash flow at 29% FCF margin and a $4.8B cash balance, Datadog is one of the rare public B2B names compounding at 30%+ at scale with elite cash generation.

Other proof points worth noting from the print:

Datadog Embraced the AI Age Better Than Almost Anyone Else

The AI Beneficiary thesis isn’t a thesis anymore. It’s showing up in the numbers. And it’s showing up in the stock chart: +66% YTD. And not just that, but at an all-time high:

The biggest winners from AI aren’t just going to be the LLM providers themselves. They’re also going to be the top picks-and-shovels B2B companies that monitor, secure, and operationalize every AI workload, alongside every traditional workload that AI is making more complex.

Like Datadog. Boom!!