The Bifurcation in the AI Market

Несмотря на то что open-source модели ИИ в 10–100 раз дешевле проприетарных, последние не теряют ценовую власть — рынок раскалывается надвое. Доля open-source стабильно держится на уровне 22–25 %, а внутри этого сегмента лидерство DeepSeek сократилось с 80 % до 40 % на фоне роста Qwen и других китайских моделей. Кодинг нашёл product-market fit: на программирование приходится 60 % использования Anthropic и 45 % xAI. Ролевые игры стали быстрорастущим потребительским кейсом — 80 % объёма DeepSeek приходится именно на них. Удержание пользователей остаётся слабым: большинство моделей теряют 60–70 % пользователей в первый месяц, хотя Claude 4 Sonnet и Gemini 2.5 Flash удерживают 40–50 %. Ключевой вывод: предприятия платят за точность, потребители не платят за развлечения — проприетарные провайдеры выиграли сегмент, который готов платить.

Despite open-source AI models being 10-100x cheaper, proprietary providers haven’t lost pricing power. OpenRouter’s data reveals a market splitting in two.

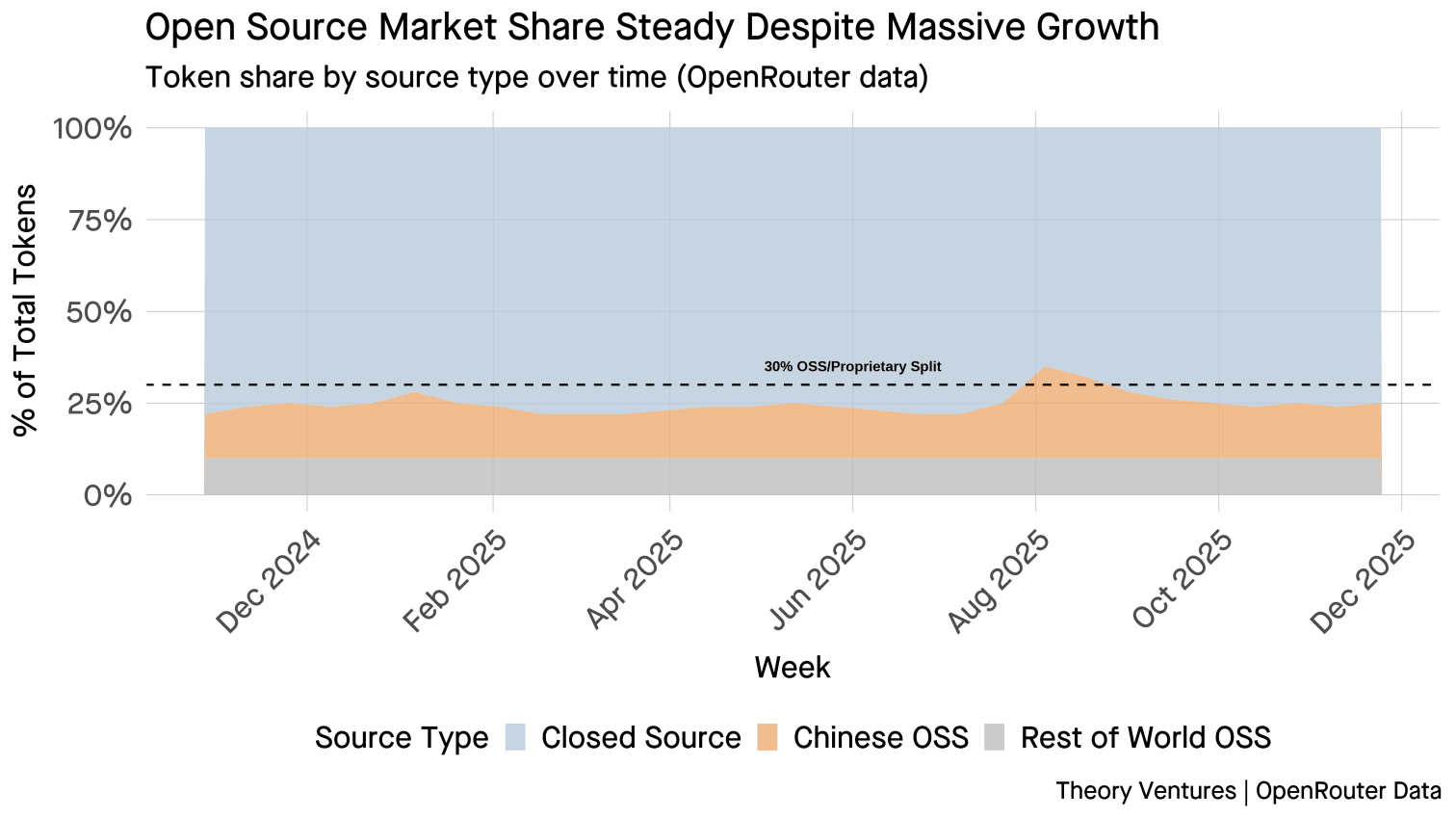

Over the last year, open-source models’ market share has remained stable around 22-25%, briefly spiking to 35% during the explosive growth of Chinese models in mid-2025 before settling back down.

The weak price elasticity indicates that even drastic cost differences do not fully shift demand; proprietary providers retain pricing power for mission-critical applications, while open ecosystems absorb volume from cost-sensitive users.

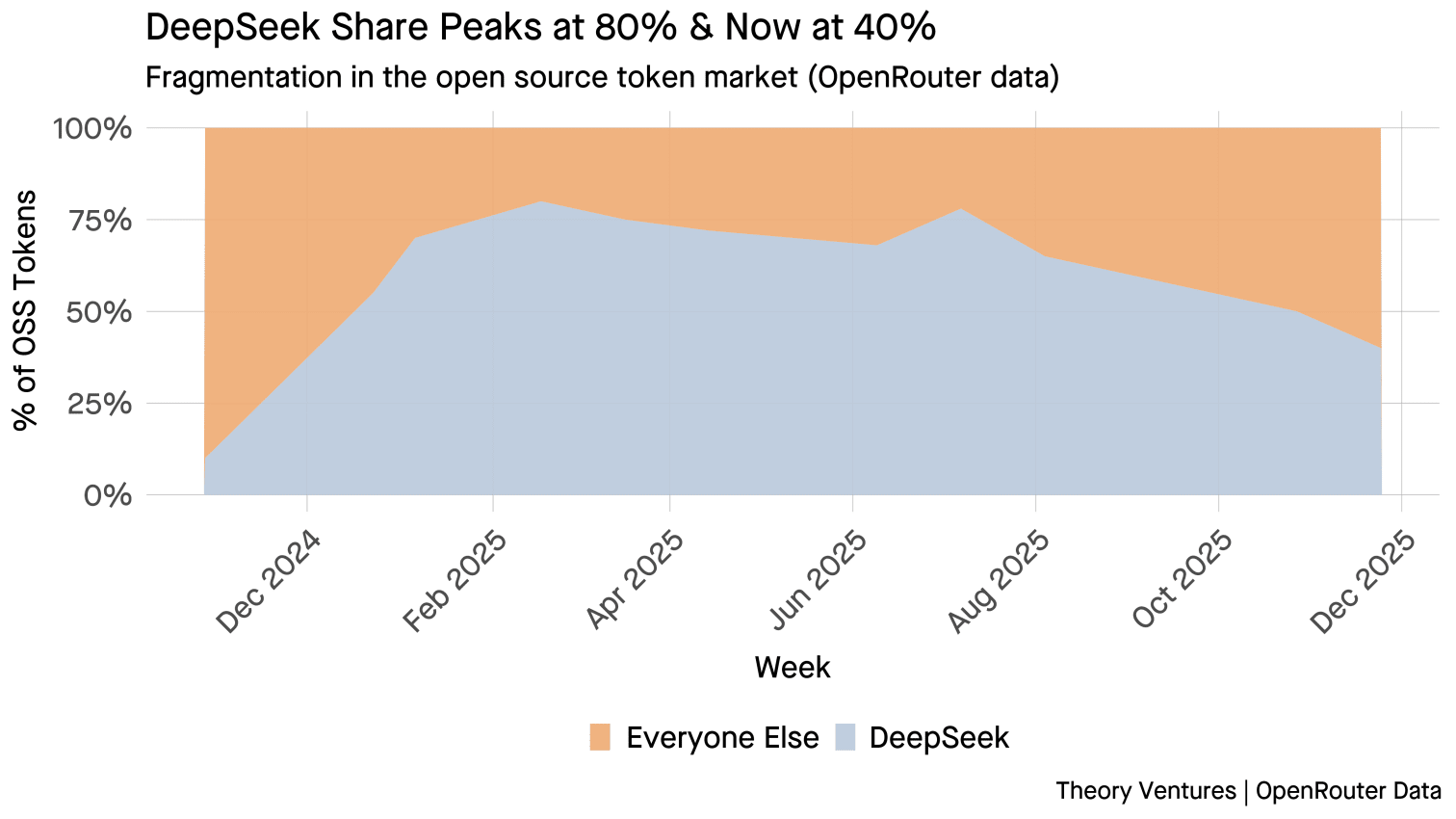

Second, the distribution of open-source models has shifted dramatically. DeepSeek held nearly 80% of OSS market share in early 2025, but has dropped to 40% as Qwen & other Chinese models have gained ground.

Third, coding has found product-market fit. Programming accounts for 60% of Anthropic’s usage & 45% of xAI’s, both heavily skewed toward developer workflows.

The table below shows the top 2 use cases by provider (November 2025). Technology refers to AI assistant tasks like research & summarization.

Role-playing is the fast-growing consumer use case. DeepSeek dominates here, with 80% of its volume in roleplay. Cost sensitivity drives this segment, so consumers won’t pay enterprise prices for entertainment.

OpenAI is the only provider with a significant fraction in science. ChatGPT’s early adoption by academics & researchers likely created lasting habits, giving OpenAI an edge in scientific workflows.

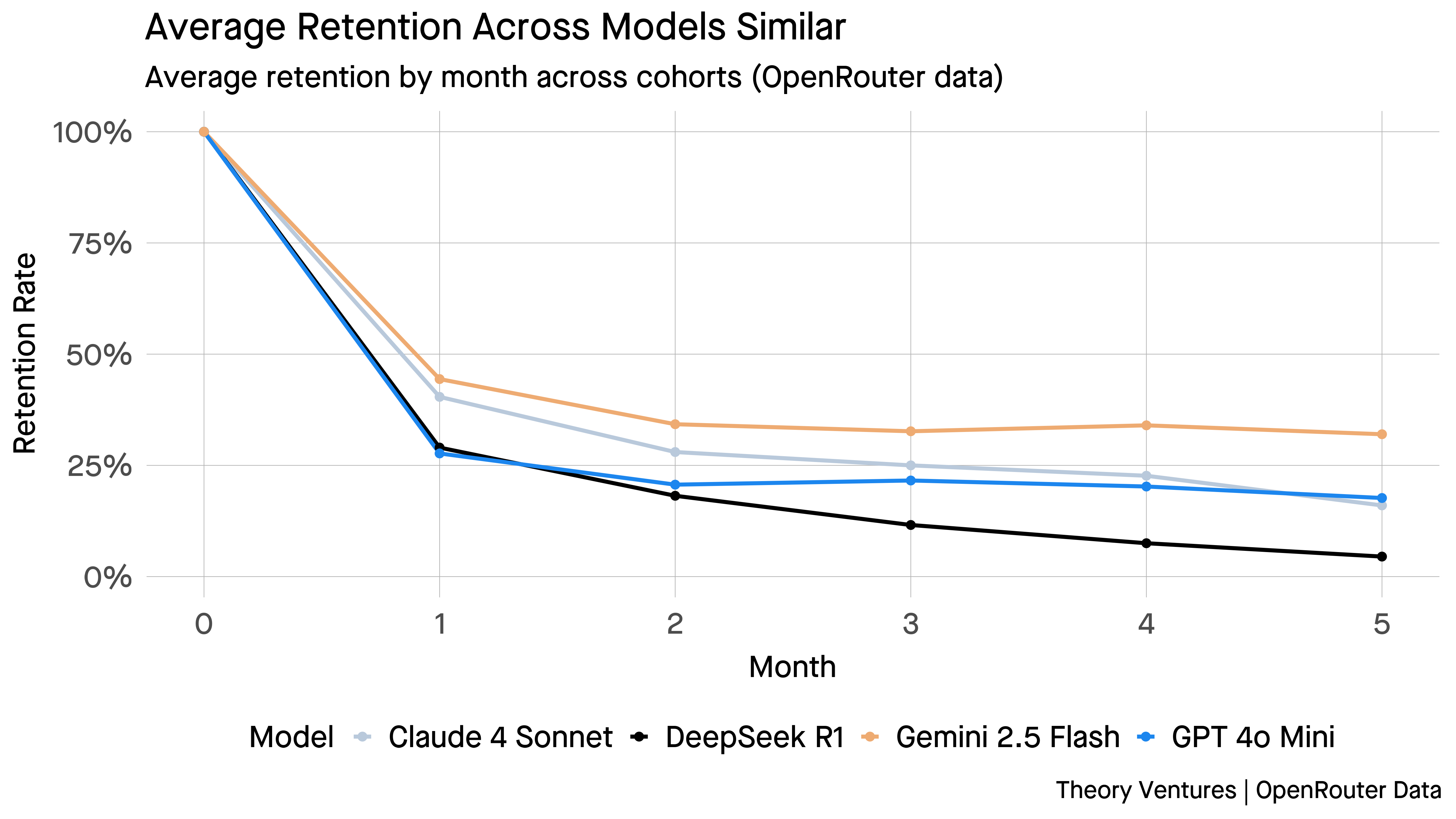

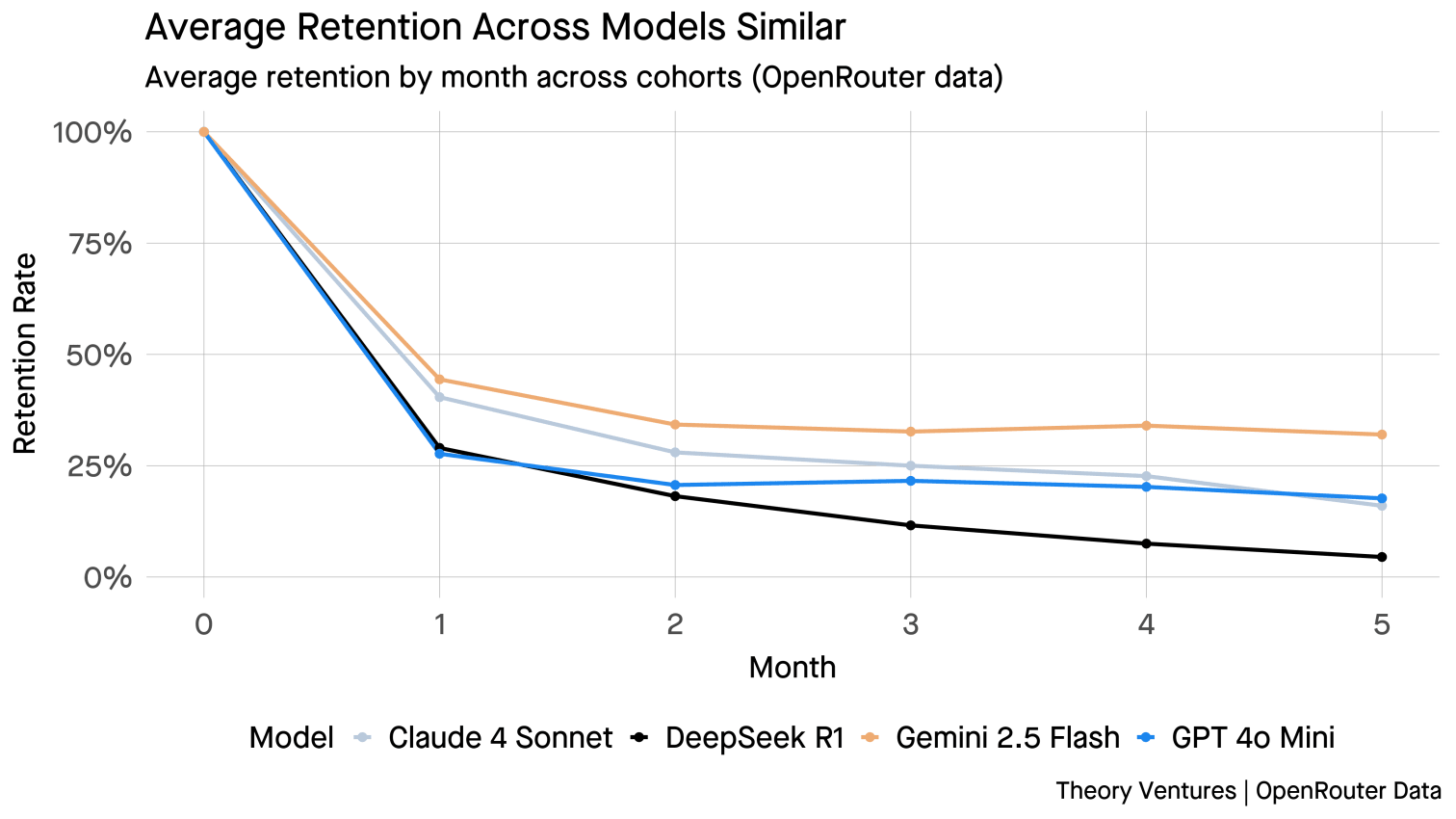

Once a model achieves product-market fit, retention improves significantly. But stickiness is rare, churn is the norm, most models lose 60-70% of users within the first month.

The chart below contrasts retention across leading models. Claude 4 Sonnet & Gemini 2.5 Flash show stronger Month 1 retention (40-50%) compared to GPT-4o Mini & DeepSeek R1 (25-35%), suggesting deeper utility for certain workflows.

The answer to the pricing puzzle : enterprises pay for precision, consumers pay nothing for play. Proprietary providers don’t need to compete on price, they’ve won the segment that pays.

Data Sources: