AI at Discount

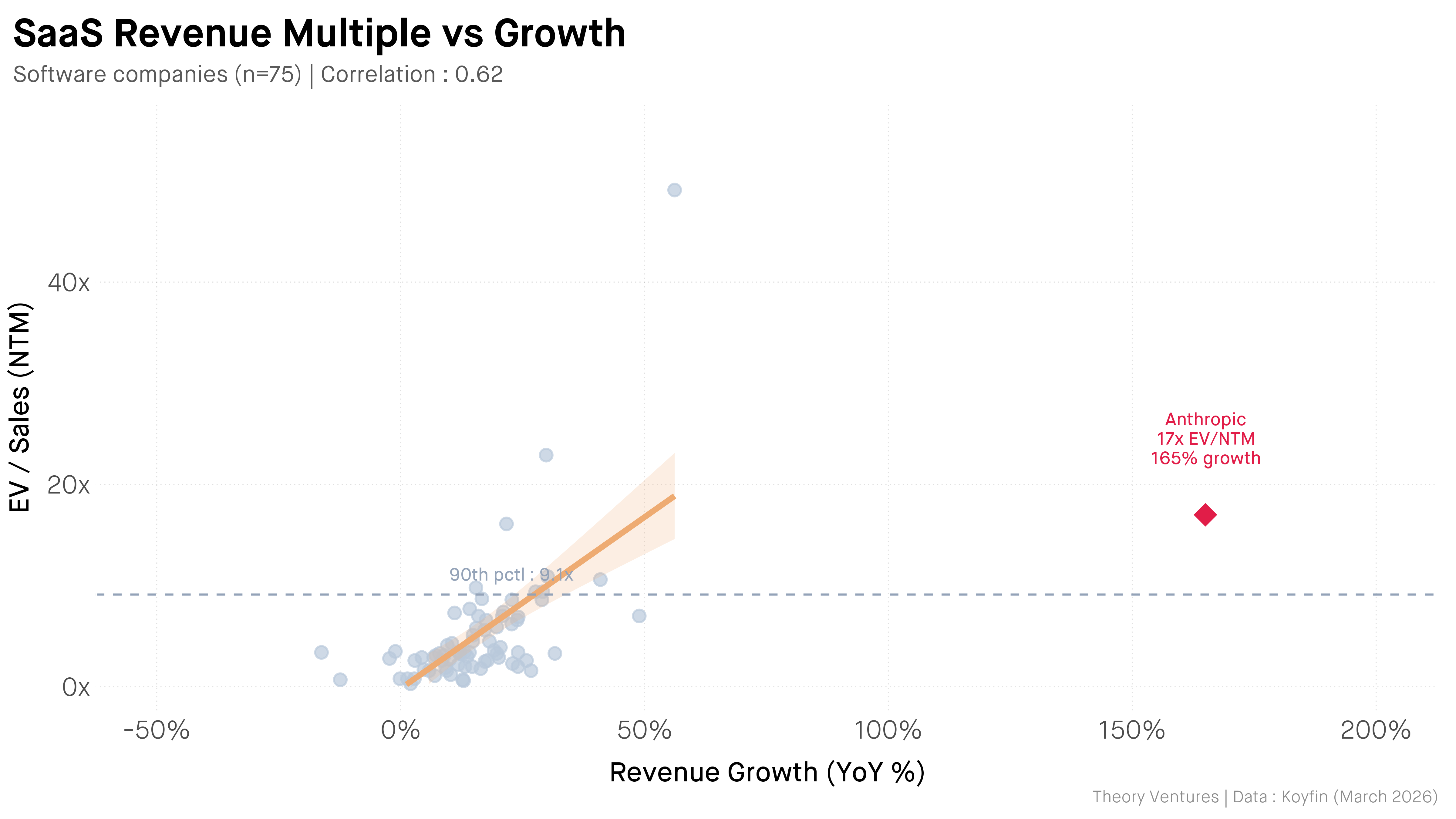

Anthropic выросла с $1B до $30B годовой выручки за 15 месяцев, но торгуется с дисконтом к публичным аналогам. При текущем run rate $30B фактическая TTM-выручка оценивается в $20B, а к концу 2026 ожидается $80B, что даёт EV/NTM около 17x — на 65% ниже Palantir при росте почти втрое быстрее. Разрыв объясняется четырьмя факторами: высокая капиталоёмкость (Anthropic привлекла $15B+, а сделка по GPU xAI Colossus обойдётся в $6.2B в год), неопределённость прибыльности (GPU составляют 60-65% capex дата-центров), волатильность роста и экзогенные политические риски от регулирования AI. Дисконт не иррационален — он отражает неопределённость в самом быстрорастущем и быстро меняющемся рынке.

Anthropic grew from $1B to $30B in 15 months. So why does it trade at a discount to public comparables?

High-growth companies trade on forward (NTM) revenue. Anthropic’s $30B run rate implies $20B in actual TTM revenue. If they exit 2026 at an $80B run rate1, we can estimate NTM revenue of around $50B. The EV/NTM multiple is 17x.

Anthropic commands a 65% discount to Palantir while growing nearly 3x faster. Four factors explain the gap.

Capital intensity. Anthropic has raised $15B+ and will need more. The xAI Colossus GPU deal alone will cost $6.2B annually at current market rates2.

Profitability uncertainty. Revenue multiples assume future profitability. GPUs account for 60-65% of AI data center capex3. Anthropic could be growing into a high-margin software business or a capital-intensive utility. The market doesn’t know yet.

Growth volatility. In March & April, Anthropic’s revenue exploded. Will that growth continue? Public markets prefer predictable growth curves they can underwrite.

Exogenous political risk. AI regulation is in flux. Export controls, compute caps, safety requirements : any of these could reshape the competitive landscape overnight.

The discount isn’t irrational : it prices uncertainty in the fastest growing & quickest changing market.

The $80B run rate is an estimate used to derive the NTM multiple. ↩︎

Using Ornn’s Compute Price Index spot rates : (150k H200s × $2.64) + (50k × $4.13) + (20k × $5.29) = $708k/hr, or $6.2B annually. ↩︎

Goldman Sachs estimates GPUs and IT equipment account for 60-65% of hyperscaler AI data center capital expenditure. ↩︎